Help Center AffiliCon

Calculation of VAT - OUTDATED - PLEASE USE THE GERMAN VERSION

OUTDATED - PLEASE USE THE GERMAN VERSION:

Berechnung der Mehrwertsteuer, OSS (vormals MOSS) & EU-Geschäftskunden

---

In which country does VAT have to be paid?

Within the EU the calculation of VAT depends on a variety of factors and is thus very complex. In the following article we will show you how different seminars, digital and physical products are taxed.

Taxation of digital products

In the case of digital products, the value-added tax applied in the respective country of the buyer has been calculated and paid out since January 2015.

The sales of all private customers in EU member states are settled by the simplified “mini-one-stop-shop-procedure" (= MOSS).

Entrepreneur (Unternehmer i.S.d. UStG) with a valid VAT-IDs on both side get an exemption according to the reverse-charge-procedure.

Example:

If a customer residing in France purchases a digital product (eBook, for example), the value-added tax of 20% is paid to the French tax authorities via MOSS.

If a customer residing in Luxembourg purchases a digital product (eBook, for example), the value-added tax of 3% is paid to the Luxembourg tax authorities via MOSS.

Taxation of physical products

In the case of physical products, we have to consider the delivery threshold of the respective countries. Up to a certain annual threshold value, the value-added tax is levied in its own country. After the country delivery threshold has been exceeded, the value-added tax of the corresponding country is deducted.

For us, this is the case with Austria, where the value added tax of 20% is deducted (10% food / books, 13% plants / cultural events).

In Germany the common value-added tax is 19%. The reduced tax rate of 7% refers to food, books, art objects and hotel overnight stays.

Example:

A customer residing in France orders a mobile phone cover to Paris. If the delivery threshold for France has not yet been exceeded, the mobile phone protection cover is deducted with the German VAT of 19%.

Taxation of seminars

The taxation of seminars in different countries is basically determined by the location of the seminars. If, therefore, the place of the seminars is abroad, the taxation of the seminars is governed by the national legislation of that country.

Example:

A German customer residing in Germany acquires a ticket for a seminar in Austria. Since the seminar takes place in Austria, it is recorded with the austrian value-added tax 20%.

Exceptions apply if the participant of the seminar is an entrepreneur (Unternehmer i.S.d. UStG) and not a private person. In that case the residence of the entrepreneur plays a role and a German entrepreneur has to pay 19% VAT while for an entrepreneur of other EU-member states the reverse-charge rule with 0% applies.

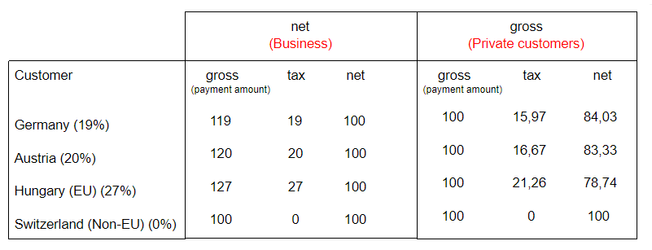

Composition of the payment amount with and without taxes:

What are the fees of AffiliCon?

AffiliCon charges 7% of the gross selling price of the product plus 1 € as a fixed amount.

Find detailed information to the affilicon fees here:

If you have any more questions, please write us via https://support.affilicon.net/contact/ or clients@affilicon.net.